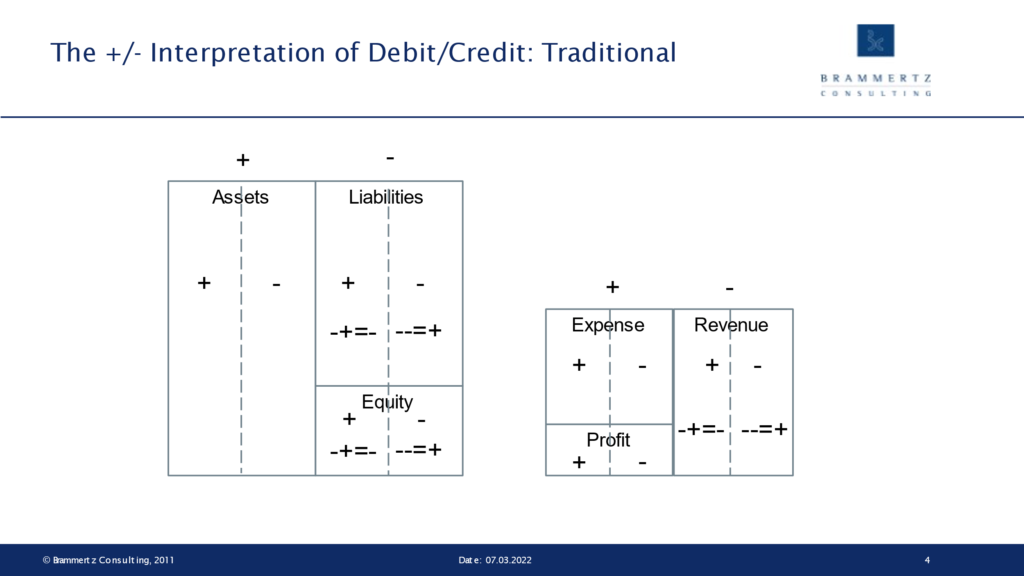

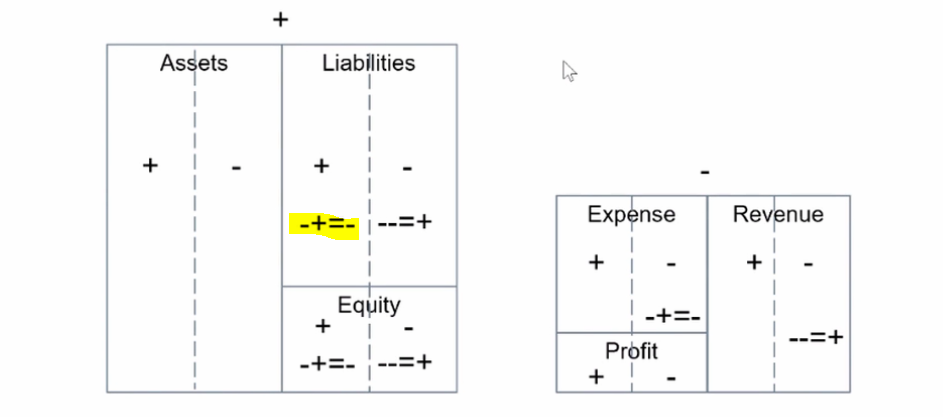

Since we begin with liquidity and track inflows as a positive value, then net cashflows off of the profitLoss statement add to cashAndCashEquivalents balance and the flip side on the balance sheet is the increase of equities through a credit adjustment to equity via retained earnings representation.

WBR: Yes, correct. I think here you take profit and equity as a residual.

The math you use for constructing contracts looked interesting. Are you aware of courseware that might allow someone to understand the math & symbols?

WBR: I hope the explanation above helps better. I don’t know of a special book on signs except mine (which however does not discuss signs in depth).

In context of constructing contracts do you have some examples of -+=- & –++ with respect to liabilities? I’m believe that a cashflow into an entity to pay off a loan reduces liability balance i.e. reduces negative polarity.

WBR: First it is important to recognize, that all financial contracts have in and outflows (Operational contracts have only an in- or an out-flow). For this reason, I say, that the sign of financial contracts are determined by the future flows. A liability has first an inflow followed by outflows (Saving and current accounts have continuous in- and out-flows but the argument still holds). With assets it is the other way round. Example of the liability, say a simple bullet bond (PAM in ACTUS language) of notional 1000: Before value date or the first flow, the future expected principal flows are +1000 and -1000 and they sum up to zero. The value is zero. As soon as the inflow of +1000 at value date comes, we have only future outflow in front of us. The value is -1000. At maturity date we have an outflow of -1000 and no future flows anymore and the value is zero. If we include interest payments (in normal time where rates are positive we have a sequence of outflows (=expenses) at each interest payment point. Operational contracts have after the first flow no contract related in- or out-flows. This means the future cash-flow is zero. For this reason, their notional value is zero and the value is represented purely by what we call PD.

we have a sequence of outflows (=expenses) at each interest payment point. Operational contracts have after the first flow no contract related in- or out-flows. This means the future cash-flow is zero. For this reason, their notional value is zero and the value is represented purely by what we call PD.